Advisory

Portfolio Advisory

Quantilution is an innovative, disruptive and adaptive Portfolio management concept that is applicable to the entire stock universe.

Innovative conventional risk models are questioned and a more modern risk approach leads to more robust results.

Disruptive the digitized selection and allocation process can be implemented extremely efficiently and cost-effectively.

Adaptive in all market cycles, a Portfolio adapts to the lowest volatility pattern.

Portfolio Managers or asset managers like to keep their cards close to the vest. On the one hand, the competition is fierce and on the other hand, similar systems are often used for decision-making. This applies in particular to risk models.

In addition, the permanent review and reorientation of Portfolio allocations can be a time-consuming and sometimes also cost-intensive process. What is the actual contribution of corporate analysts or quantitative trading models when only a small minority of asset managers are able to beat a benchmark over a long period of time? However, the purchase of ETF'S or the use of Robo-Advisor cannot be the solution if you want to distinguish yourself from competitors.

An innovative, disruptive and adaptive approach must go deeper. It must take up innovations and question the traditional. This challenge Quantilution has taken on and it provides a solution.

Quantilution works with a novel and sustainable risk concept, which provides measurable performance advantages over conventional portfolio approaches.

Quantilution quantifies the psychological behavior pattern in stock markets using volatility clusters and derives clear risk and return profiles for Investments from this. Holding loss positions is avoided.

Quantilution delivers a fast and cost-effective decision basis for the selection of solid and successful listed companies worldwide.

Quantilution has developed a long-term Portfolio strategy based on this and which has a Beta of at least 1 in positive market cycles and a Beta significantly smaller than 1 in negative cycles, which corresponds to implicit hedging. This strategy has been in real trading mode since October 2016.

Returns are not predictable.

Prof. Robert Engle

Volatility is clustered

Prof. Robert Engle

Volatility is asymmetric

Prof. Robert Engle

Return/Risk can correlate negatively

Prof. Robert Engle

Analytics

Portfolio Analytics

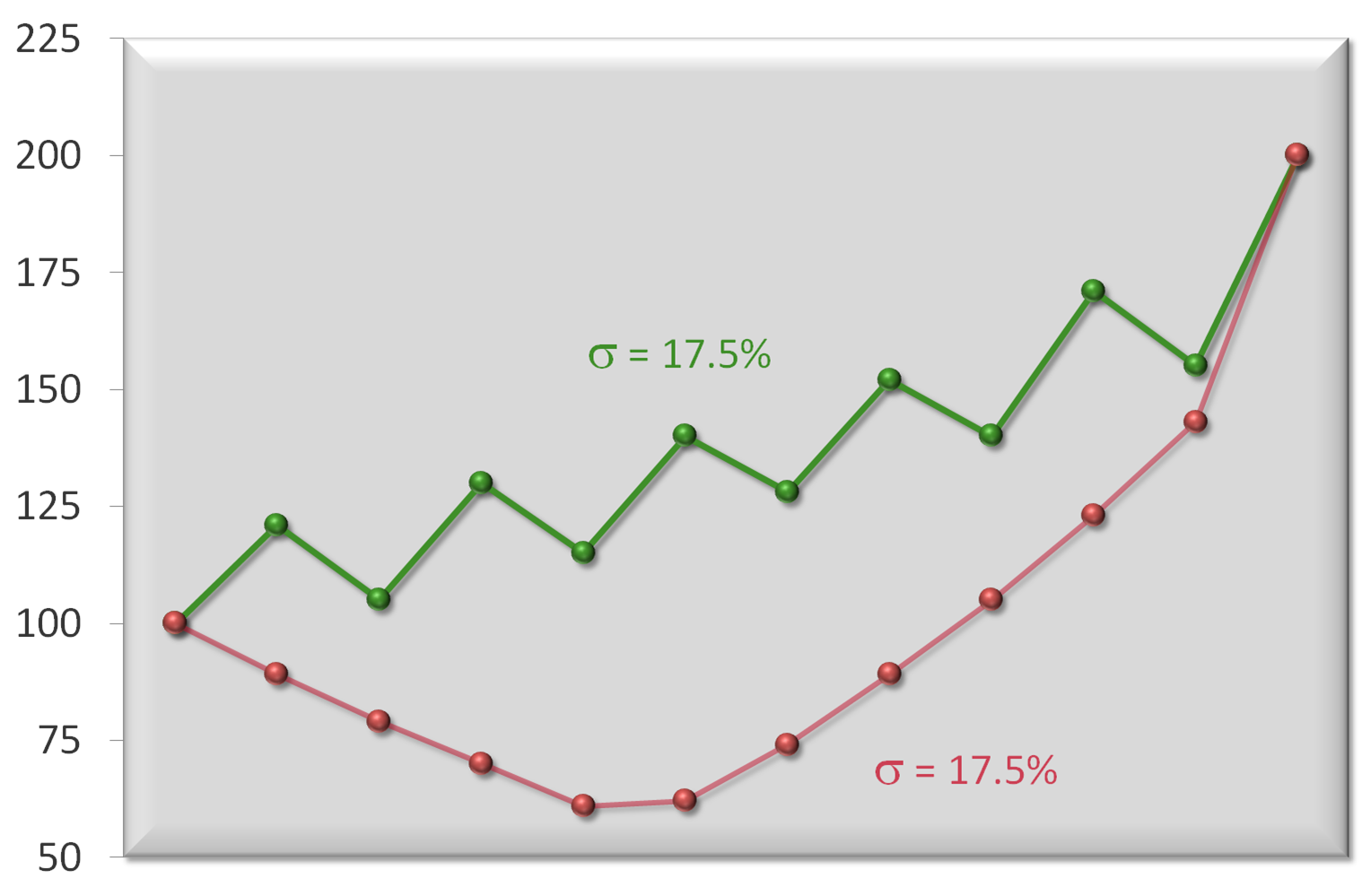

Risk measurement is absolutely essential for a qualified Investment analysis. Conventional measures such as the standard deviation σ do not accurately capture the actual volatility structure of a time series. Quantilution has developed, based on the results of the 2003 Nobel Prize winner, Robert Engle, a new method, the Volatility-Cluster-Machine (VCM), which divides risk into a price and time component. This two-dimensional approach leads to more precise risk statements. In the adjacent Chart, only one of many examples is listed, which mathematically evaluates both curves in terms of volatility and thus also Sharpe Ratio equally. The VCM measure, on the other hand, measures a significantly lower risk and thus higher stability for the green curve.

Click to enlarge

With the more precise risk measure, volatility clusters, which can be empirically proven in all time series, are determined very precisely. The advantageous property of a cluster is the structure similarity within an indefinite runtime. Meanwhile, the predictability of volatility and thus stability is highest.

Quantilution has developed for this analysis the VCM algorithm (Volatility-Cluster-Machine algorithm) . It identifies the most recent time variable cluster and classifies it according to its stability structure. In particular, the volatility asymmetry is taken into account, which statistically describes a lower fluctuation range in a rising market and a higher volatility in falling markets.

With the determination of volatility clusters for each investment, a hierarchical classification is possible. For example, investments are preferred that are located in clusters with low volatility and positive return and therefore have a relatively high stability. Risk management consists of evaluating the cluster structures. In particular, this minimizes the risk of negative correlation between return and volatility that can occur if a risk threshold is exceeded. A portfolio compiled according to these criteria is superior to an “efficient” portfolio according to Markowitz, especially in times of stress.

The Quantilution strategy can be implemented with any stock universe. A portfolio consisting of 10 to 50 shares is always invested and avoids any timing. The strategy responds to changing sector rotations which occurred particularly clearly in 2020, but are also increasingly prevalent in bear markets, by quickly switching to the most stable clusters, thereby avoiding up to 50% of the bear market, especially the longer it lasts.

View Current Portfolio

years test period

Sharpe-Ratio

Transactions per Month

Months average holding period of a stock

Results

The successfully implemented analysis of the Volatility-Cluster-Machine is the basis for an active and opportunistic Portfolio strategy since autumn 2016. Quantilution shares this approach and offers consulting and investment solutions. Request the results and a personal presentation and get to know the advantages of a more modern and robust risk approach for Portfolio Management without obligation.

Media

Press

«Quantilution sees alpha in volatility clusters»

15 March 2021

16 July 2020

*Note

Ethius Invest GmbH should not be confused with Ethius Invest Schweiz GmbH, which does not have a license for the strategy described.

«Ethius Invest takes inspiration from Robert Engle to limit volatility»

22 April 2020

*Note

Ethius Invest GmbH is not to be confused with Ethius Invest Schweiz GmbH, which does not have a license for the “Warren Machine”. The author of this website, Martin Rothe, is the sole author of the “Warren Machine”.

28 January 2020

*Note

Ethius Invest GmbH should not be confused with Ethius Invest Schweiz GmbH, which does not have a license for the strategy described.

Contact

Contact

ABOUT ME

I have extensive experience in Portfolio Management, particularly in the field of quantitative trading, and have in-depth knowledge in risk management, which I studied extensively during my 25 years as an Investment Fund Manager. Furthermore, I research data models that transform Portfolio Management into the digital age.

I worked at Man Group in Switzerland in Financial Engineering and smaller Hedge Funds in Switzerland and London. I was institutional fund manager at private bank Schröder, Münchmeyer, Hengst and Commerzbank in Frankfurt and got my basic training with Swiss Bank Corporation in Zurich, Basel and New York. I am a business economist from Goethe University in Frankfurt.

Martin Rothe

CONTACT

Privacy Policy

Cookies Policy

Copyright © Quantilution 2020